Imagine being in a career that gives you a clearer, faster path to early retirement. Not the traditional timeline where you wait until your 60s, but one where you can realistically move that date up by 15 to 20 years, even if you’re starting with zero invested today. And even if you never plan to fully retire, picture having the freedom to make work optional instead of necessary.

That’s the idea behind Financial Independence (FI). For a long time, FI and early retirement felt like something only available to high-earning executives, business owners, or people willing to adopt extremely frugal lifestyles for decades.

Over roughly the past five or six years, though, one career path has emerged as a surprisingly powerful accelerator toward FI: working in the Salesforce ecosystem.

Between above-average compensation, steady market demand, and flexible income options like freelancing or fractional roles, Salesforce professionals have an unusual level of influence over the two biggest drivers of an FI timeline… how much you earn and how much you spend.

The video below is a great companion for this article with additional details and insights.

What is Financial Independence

If you’re like most people, you might be thinking, “Okay, early retirement and financial freedom sound great… but what exactly is Financial Independence?” You may have heard the phrase before without ever really digging into what it means.

Financial Independence simply means having enough invested assets that your money can cover your living expenses indefinitely. Not just for the next few decades, but for the long term without you needing to rely on a paycheck.

At that point, your investments are doing the heavy lifting through compound growth. Some people like to think of it as a perpetual income engine, a system that keeps generating money on its own. And yes, it can even be passed down, but that’s a deeper topic for another day.

Before we get into the numbers (don’t worry, the math is simple), there are a couple key terms to understand.

- Financial Independence Number or FI Number – This is the amount of money you need saved to no longer need money for the rest of your life, to build your Perpetual Money Making Machine, to retire, to reach Financial Freedom.

- Annual Expenses –This is how much you spend each year.

The most widely used way to calculate your FI Number is straightforward:

25 x Annual Expenses = FI Number

If you finish this article and the math still isn’t mathing, I highly recommend this article for a more descriptive breakdown of the math behind Financial Independence and Early Retirement. First, finish this article so you understand why being in a Salesforce career uniquely predisposes you to reaching your FI number in fast forward.

Let’s look at a realistic example that you can apply to yourself:

If annual expenses are $78,000 per year (roughly the U.S. national household average), we can apply the formula:

25 × $78,000 = $1.95 million

So in this scenario, your FI Number would be $1.95M.

That might feel like a big number at first glance. But once you understand how saving and compounding work together over time, you start to see that FI is far more about consistency and income growth than it is about luck.

And importantly, many people don’t actually stop working when they reach FI. Instead, they reach a point where work becomes optional, meaning they can choose what to work on, how much to work, or whether to work at all.

The Two Levers to Control & Shorten Your FI Timeline

Income and expenses are the two main variables that ultimately determine how quickly you reach Financial Independence.

For most households, spending is heavily concentrated in what’s often called the “Big Three”:

- Housing (rent or mortgage)

- Transportation (car payments and related costs)

- Food (groceries and dining out)

While both sides of the equation matter, this article will primarily focus on income growth and how it can dramatically accelerate your FI timeline, especially with a Salesforce career.

That said, it’s still important to take a close look at your spending. Adjusting expenses can significantly influence how soon you reach FI. The objective isn’t to cut costs to the point of feeling restricted; it’s to make intentional, value-based decisions about where your money goes so it aligns with the life you actually want.

Salesforce Careers & Your Financial Independence Timeline

Income & Expense Standards

To start mapping out a realistic FI timeline, the first step is figuring out how much you can actually save each year. Reaching your FI Number doesn’t happen by chance; it comes from consistently setting money aside and letting compounding interest do its work over time. It’s a perfect example of delayed gratification paying off.

For our baseline, we’ll use two broad benchmarks: the average Salesforce salary and the average household spending in the United States. With those numbers, we can estimate a typical savings range and begin to see how a potential FI timeline takes shape.

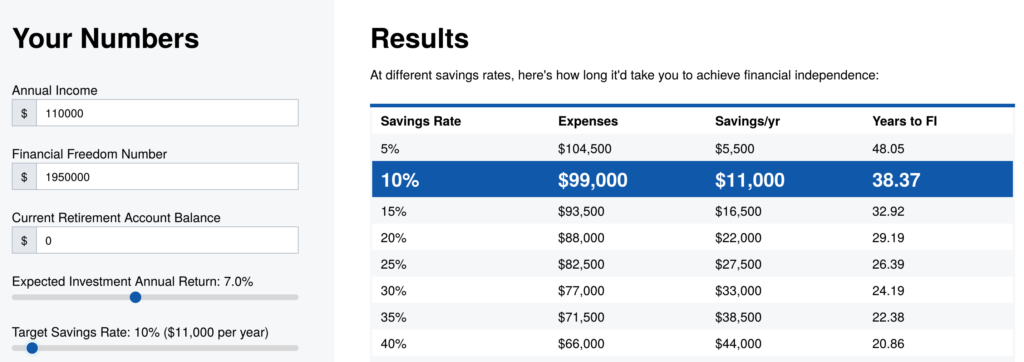

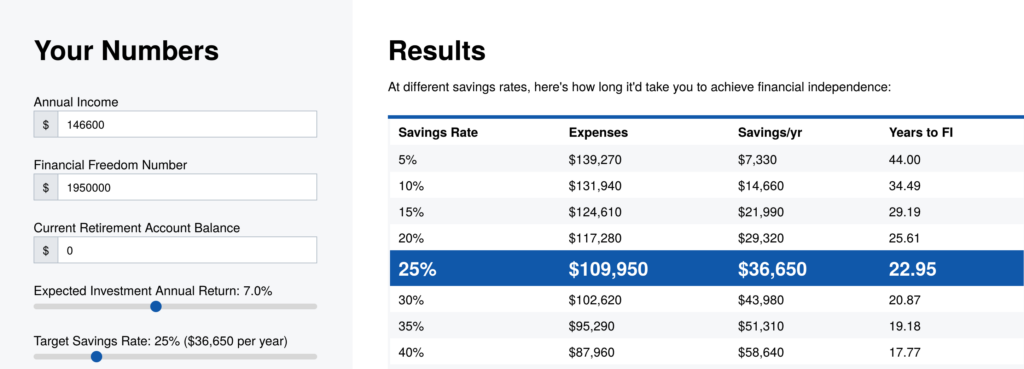

Average Salesforce professional salary (U.S., 2025): about $110,000 per year

(This spans roles like admins, business analysts, consultants, and developers.)

Average annual U.S. household expenses: about $78,000 per year

How Much Can We Save?

At first glance, it looks like we can simply save $32,000 per year. However, we need to calculate for taxes and deductions, which lowers our true Savings Potential to $10,000–$12,000 annually, depending on tax optimizations. Let’s meet in the middle and call our Base Savings $11,000.

This is exactly why increased income via raises, promotions, or freelancing becomes such an impactful catalyst for Financial Independence.

Investment Growth Estimates

Once we’ve set money aside, it doesn’t grow well in a piggy bank or under the mattress. To reach Financial Independence, we need our savings to work for us; after all, this is how we build the Perpetual Money Making Machine.

The key is investing, but it doesn’t need to be complicated or risky. Keeping it simple is the best approach, especially when you’re just starting out.

A broad, low-risk index fund like the Vanguard Total Stock Market Index Fund (VTSAX) has historically delivered about 7% annual real return (after accounting for inflation) over nearly 100 years.

With our annual expenses, income, and a realistic expected rate of return in mind, we can now estimate our Timeline to FI and see just how much our choices can speed up or slow down that target date.

Time to FI with No Raises or Income Increase

FI target using $78k average US annual expenses:

$78,000 × 25 = $1.95 million

With $11,000 in Savings towards Annual Investments with a 7% Real Return your Time to FI is ~38 Years.

This assumes you have $0 saved today.

This reflects a more typical path for professionals who rely on salary alone, without having the income acceleration levers available to those with Salesforce careers.

Time to FI With Standard Expected Career Growth

If we assume a 5% annual raise (very realistic in Salesforce careers) Time to FI drops to ~34 years

So career progression alone shortens the timeline by about 4 years, even without lifestyle or career strategy. This is great news, but if you’re like me, you know we can do better. 34 years is a long time, and while there is more to life than Financial Independence, it’s definitely meaningful, and we can shave years off of this timeline.

The Fun Part 🎉 The Salesforce Fast Track!

The single biggest lever Salesforce pros have to increase their income is having a freelance side client. This may sound minimal at first, but just wait until you see the numbers play out. It’s absolutely mind-blowing.

Freelancing has so many benefits in addition to helping with our FI goals. We create a broader network, learn skills and processes beyond our day job, grow as small business owners, and diversify our income. With that in mind, let’s look at the impact of Salesforce Freelance Clients.

Example 1 – One Small Salesforce Side Gig

Let’s assume this client is small; we don’t want to overwhelm ourselves. Heck, in a perfect world, we can manage this client during our lunch breaks and maybe one extra work session in an evening or on the weekend. Sure, it’s a sacrifice, but let’s see if it feels worth it.

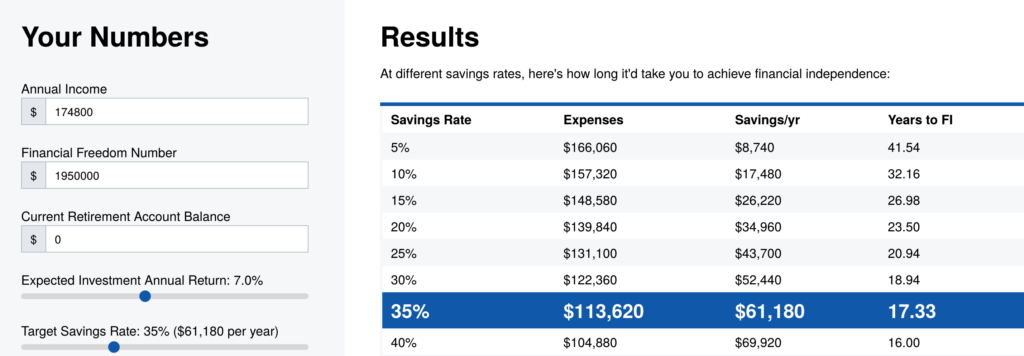

Let’s say we get a client locked in at 30 hours/month. That’s about 1 hour per day. Let’s also assume we charge a middle-ground Salesforce freelance consulting rate of $85/hour.

$85/hour x 360 hours/year = Annual Income Increase: $30,600

After taxes and deductions, that’s about $23,000 in income that can go straight to savings. This assumes we use no tax strategies like pre-tax accounts, etc., so in reality, we can save even more, but let’s keep it simple. We can always dial in the margins once we have our foundations in place.

Updated Savings is now 🤯

$11,000 (Base Savings) + $23,000 (Freelance Savings) = $34,000 in Annual Savings

With $34,000 in Savings with a 7% Real Return your Time to FI is ~23 Years.

This one change, one extra hour per day just shaved 15 years off of your Time to FI. Isn’t that unreal?

Example 2 – Two Small Side Clients – A Natural Freelance Progression

Let’s assume that we’ve been working with client 1 for a few months. Things have settled in, we understand their business, we have our challenges, but it’s more routine. We’re excited as we watch our savings skyrocket. We feel more free, we feel more in control, and options are opening up. We’re motivated and decide to layer on just one more client.

Let’s say we get another client locked in at 30 hours/month. This one again is $85/hour; however, with client 1, we are now more valuable. We know their business; we work faster, they don’t have to explain as much, and they know our work ethic and value. So we raise our rate to $95/hour (still very reasonable and arguably low).

Client 1 Income: $95/hour x 360 hours/year = Annual Income Increase: $34,200

Client 2 Income: $85/hour x 360 hours/year = Annual Income Increase: $30,600

Total Annual Income Increase = $64,800

After taxes and deductions, that’s about $48,600 in income that can go straight to savings. This again assumes we use no tax strategies like pre-tax accounts, etc., so in reality, we can save even more, but let’s continue to keep it simple.

Updated Savings is now 🤯

$11,000 (Base Savings) + $48,600 (Freelance Savings) = $59,600 in Annual Savings

With $59,600 in Savings with a 7% Real Return your Time to FI is ~18 Years.

We’re definitely hustling now, two extra hours per day, but we just shaved another 5 years off our our Time to FI. Now Reaching FI a full 20 years faster.

Why Freelancing, FI and Early Retirement are so Synergistic

Many people pursue early retirement because they want more time, less stress, and more autonomy.

Salesforce freelancers often realize they don’t actually want to stop working. Once they have more control over their time, they feel far less pressure to retire early. It’s very common to see freelancers quit their day job and keep 2-4 small clients.

Working 15–30 hours per week while earning a strong income creates a lifestyle that already feels close to FI long before hitting the actual number. Salesforce freelancers find they have more time with family, more time for hobbies, and more time to travel, all while experiencing continued professional growth.

What’s Next & Where To Learn More

Now it’s time to decide if this is something you want to implement in your career and life. Is the outcome compelling enough to warrant the inputs for you?

If the answer is No, then you can exit out of this article and simply move on with your career 🙂

However, if the answer is Yes, then you need to take action right now. This will not happen by accident, this will not happen tomorrow, next month, or next year through sheer desire. This will happen because you take action starting now.

Here’s How You Can Take Action Right Now

- Calculate your annual expenses.

- Calculate your FI number (Expenses × 25).

- Calculate your savings rate (Annual Income – Annual Expenses).

- Estimate your FI date using a calculator. (Here’s the one I used for this article)

- Get Your 1st Freelance Client – Not sure how? Start with this Free Freelance Guide.

Watch Salesforce Career focused videos, listen to podcasts and check the menu items above for links to free content and courses.